Checking your credit score can either be anticipated with great apprehension or become a badge of honor but nearly all of us need to have a decent score. These 3 little numbers can determine whether you're able to buy the house of your dreams or move into yet another high priced rental.

According to the National Association of Realtors, just 12% of home buyers in 2017 paid cash for their home. So, the vast majority of us at some point in our life will need to get a mortgage. Although lenders look at your income, debt, and cash, your credit score is one of the first things that they check to determine if you can get a loan since your score plays such a big role in the mortgage process. They need to protect their own interests so lenders use your credit score to find out "how likely" you are to pay them back.

Common Questions About Credit Scores & Mortgages

- Is my score good enough to obtain a mortgage?

- What's the lowest score to get a loan?

- What's the average score?

- Does a high score guarantee the best rate?

- What's the difference in price between having good or bad credit?

Ok, you have these questions bouncing around in your head but you have no idea of what your score really is so don't make it a mystery any longer. There are some great, reputable companies online that we have at our disposal and we can use them any time we want to check our credit score for free. You have to start somewhere and it's best to not have any surprises when you talk with a mortgage lender.

Check Your Credit for Free:

Wallethub

Credit Karma

Credit Sesame

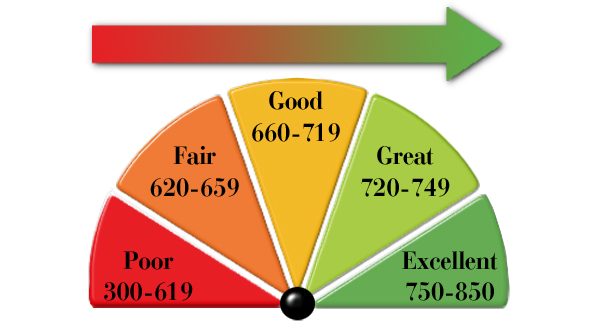

As mentioned earlier, your credit score isn't the only factor in getting a mortgage. You could have a score of 810 but your income level is too low or have a 725 with no money in savings. However, if you have a good job, little debt, and enough cash for at least a down payment here is an idea of how your credit score can effect your interest rate.

- Excellent (750-850) - Your score will have no impact at all on your interest rate and you're likely to be offered the best rate possible.

- Great (720-749) - With this score your rate will be minimally effected with an increase of around 0.25% over the best rate.

- Good (660-719) - Your rate will be effected about 0.5% higher than the lowest available.

- Fair (620-659) - Your rate will have a definite impact with an increase of up to 1.5% above the lowest possible.

- Poor (300-619) - You will pay the highest interest rates possible.

This is just a rough idea of how your score can impact your rate and the increase over the best possible rate could vary depending on the company. However, you are able to see that you'll pay for having a lower score.

What Score is Needed to Buy a Home?

You would think that the answer would be "cut and dry" but it really depends on what type of mortgage you want. No matter what type of loan you get, having the highest possible score will guarantee you the best interest rate resulting in saving you a lot of money over the life of the loan. However, home buyers with lower scores can still get a mortgage so this article will focus on the bare minimums.

If you have bad credit but still want to buy a house, an FHA loan will be your best bet. FHA loans have the lowest credit requirements for any other mortgage. If your credit score is between 500-579 you can qualify for an FHA loan if you have a 10% down payment. If your score is 580 or higher your down payment can be reduced to 3.5% for FHA. Also, there are no minimum or maximum requirements to obtain an FHA loan. While it's not impossible to qualify for an FHA loan if your score is 579 or below, you will more than likely be approved at 580 or higher.

Here are the typical minimum FICO scores for the various mortgage loans:

- FHA Loan - 580+

- USDA Loan - 640+ (Read about USDA loans here)

- Va Loan - 620+

- Conventional Loan - 620+

So there it is - the bare minimum credit score that you need to get a mortgage. Now, as mentioned earlier, there are other factors that come into play as well that can help balance out the scales for lower credit scores. Lenders aren't so closed minded that they just look at the score, then make a decision, yes or no. Have you recently re-established credit over the last 12 months? Was there a significant event that caused your score to be lowered? Do you have a high income? Is your debt to income ratio low? Have you recovered from a financial hardship? Do you have a high down payment? Do you have a recent payment history with no late payments? Have you been employed by the same company for a long time? These are all questions that a lender will consider if your credit score is less than desirable.

Do you need to work on your score? Here's a list of the best credit repair companies for this year!

Buying a home with a low credit score can be challenging but you do have options. There are also things that you can do now to improve your score in order to get the best possible rate in the near future. Please read the other articles below for other tips to get your credit score mortgage-ready.

Other Helpful Articles About Your Credit Score

Check Your Credit Score Before Buying a Home - Maximum Real Estate Exposure

12 Tips to Improve Your Credit Score to Buy A Home - Kyle Hiscock

Tips for Boosting Your Credit Score - Bankrate

Ultimate Guide to Buying a Home - Live Gulf Shores Local

About the author: The above Real Estate information on What Credit Score You Need to Buy a Home was provided by Jeff Nelson of IXL Real Estate – Eastern Shore. Jeff can be reached via email at jeff@livegulfshoreslocal.com or by phone at 251-654-2523. Jeff has helped people move in and out of properties for nearly 13 years.

Thinking about selling your home? I have a passion for Real Estate and would love to share my marketing expertise!

I service Real Estate sales in Baldwin County including the cities of Spanish Fort, Daphne, Fairhope, Foley, Gulf Shores, and Orange Beach.